Jane Fraser Turned Citigroup Inside Out.Now Comes the Hard Part.-By Andy Serwer and Rebecca Ungarino, BARRON'S

The Fear of 13 is a new play on Broadway starring Adrien Brody about a man wrongly imprisoned for murder. Brody’s character passes his time learning new words, including “triskaidekaphobia,” the fear of the number 13.

A few miles away at Citigroup headquarters in lower Manhattan, employees may be all too familiar with triskaidekaphobia, as the long-beleaguered bank works through its 13th restructuring. The previous 12, the blunt-spoken Wells Fargo analyst Mike Mayo notes, “failed.”

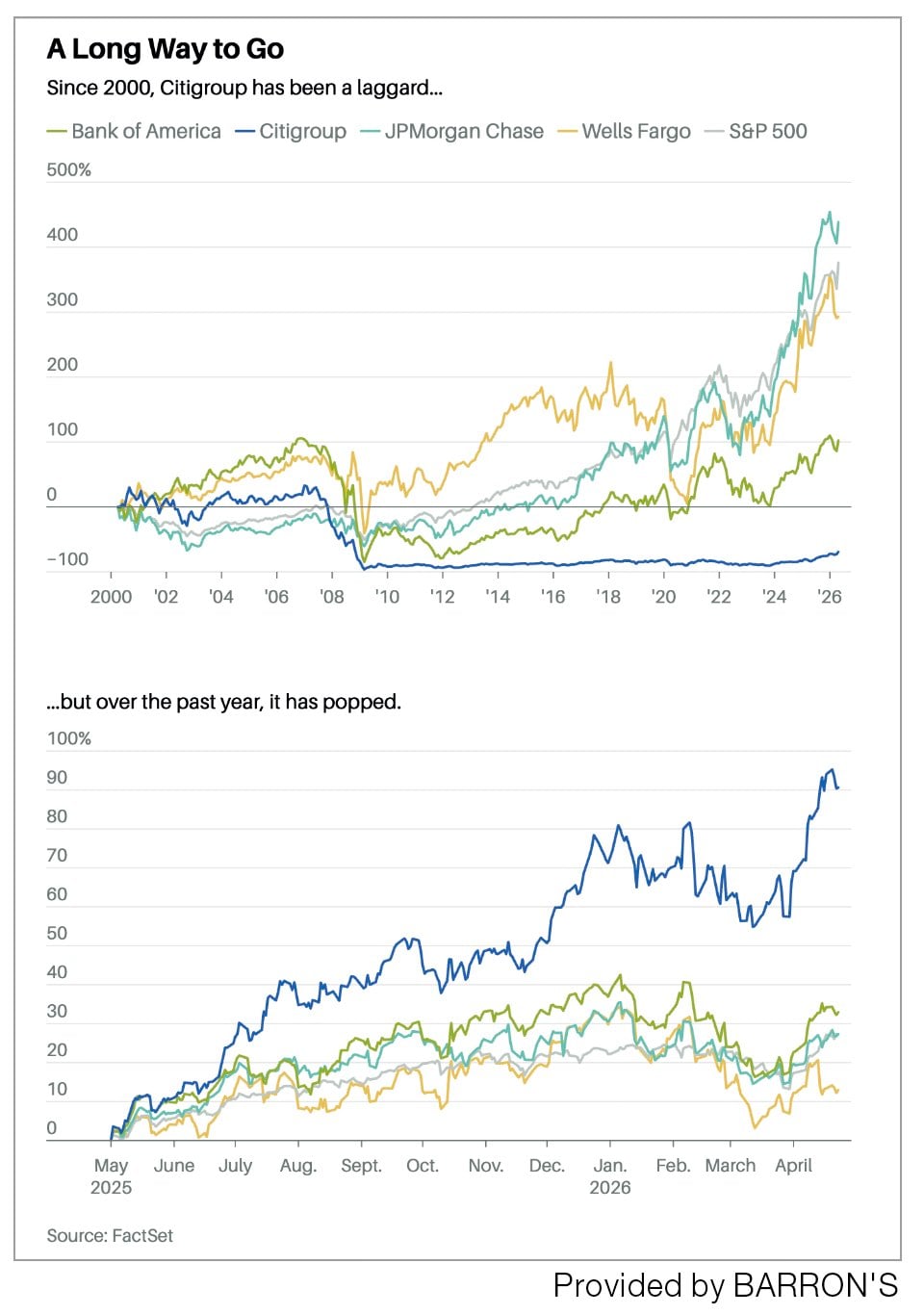

Not to disabuse a Wall Street truism, but this time might be different. Indeed, Mayo has had an Overweight rating on the stock since 2018, and at $130, Citi shares finally trade above their book value. And don’t look now, but Citi’s stock is up 161% over the past three years, crushing the performance of rivals Bank of America , Wells Fargo , and JPMorgan Chase , as well as the S&P 500 index.

Going back to the 2008-09 financial crisis, however, the stock has been an absolute dog—essentially a two-decade wealth-destruction machine. It is that lingering perception that speaks to Citi CEO Jane Fraser’s charge: She must prove to her employees, customers, and investors that the recent run-up in the stock and rebound in its businesses are sustainable and that Citi is really, truly back.

Fraser doesn’t dwell on the past. “That was decades ago,” she says when asked about Citi’s dark ages in a recent interview at the bank’s offices. “My eyes are on the destination. I see a lot more runway ahead that’s independent of where the world heads. I’m delighted to see the improvement in the performance, but there’s no victory lap.”

As part of that future-forward mind-set, Fraser and her team are prepping for the bank’s May 7 investor day and “laying out a very clear path,” she says. Doubtless she will accentuate Citi’s improving return on tangible common equity, or RoTCE—widely considered to be the so-called truth metric of a bank’s health—which hit 13.1% in the first quarter, catching up to its peers. (JPMorgan’s 23% is the high for the group.)

Another milestone will be winding down federal consent orders imposed six years ago when regulators became fed up with Citi’s weak internal controls. Fraser says the work is 90% done, and analysts will look for the feds to give the all-clear sign.

(圖片來源:資料圖片)Still, Fraser, who was named CEO five years ago and chair this past fall, knows she has more tough calls ahead—ones her predecessors failed to make, such as cutting costs, jettisoning units, reorganizing divisions, purging underperforming employees, and attracting aggressive talent.

“It’s been a very good turnaround story, but now we go from turnaround to growth, and it’s not a cakewalk,” says RBC Capital Markets analyst Gerard Cassidy. “It’s going to be a lot of hand-to-hand combat with the competition.”

Fraser herself has gone through a transformation over the past half-decade, from an executive known mostly as the first woman to run a major U.S. bank to a now-familiar, public-facing Wall Street leader. A proud Scot—“I’m Scottish and cheap,” she says—Fraser had the most Scottish of upbringings (caddying at St. Andrews and a father who was an accountant and chief financial officer). Still prone to Britishisms like “dillydallying,” the Goldman Sachs and McKinsey alum has a countenance that modulates between cheery and dead serious.

That carrot-and-stick mien probably serves Fraser well as she looks to revive the bank. With $2.8 trillion in assets—the nation’s third-largest bank after JPMorgan and Bank of America—Citi is still a behemoth, but diminished from several decades ago when it was the world’s biggest and, some would say, pre-eminent bank.

What precipitated such a fall from grace?

Citigroup’s decline, and the entirety of its 200-year history, is a story rich enough for a Ken Burns documentary. From its beginnings, Citi’s growth mirrored the trajectory of the U.S. Founded in 1812 as City Bank of New York, its early-1900s international expansion ultimately spawned its modern-day tagline, “The world’s most global bank.” Then it endured the 1929 market crash and Great Depression, initially under bank Chairman “Sunshine Charlie” Mitchell.

Citi was innovative, too. In 1961, it became the first U.S. bank to issue certificates of deposit, an endeavor led by an ambitious banker named Walter Wriston, who became its highly influential CEO. In 1977, Citi popularized ATMs, which served its customers well during the Great Blizzard that year, prompting the slogan: “Citi never sleeps.”

The bank both drove and rode waves of financial deregulation—exhibit A being its $70 billion 1998 merger with Travelers Group, which had cobbled together an amalgam of Wall Street firms including Salomon Brothers, Smith Barney, and Shearson Lehman Hutton. Combined into the renamed Citigroup, this “financial supermarket” was run by Citi’s John Reed and Travelers’ Sandy Weill—along with Weill’s protégé, Jamie Dimon, whom Weill later pushed out.

The conceit of Citigroup—in which a Citi checking account customer would buy Travelers insurance and use a Smith Barney broker—never panned out. What resulted instead was a dysfunctional Frankenbank with warring factions and disparate technology platforms, which hobbled the bank for decades.

That made Citi particularly vulnerable when the 2008-09 financial crisis hit. It held billions of dollars of collateralized debt obligations—complex bundles of subprime mortgages—as well as rapidly depreciating, off-balance-sheet structured investment vehicles, $49 billion of which had to go on its balance sheet. Through a subsidiary, Citi was one of the largest lenders to subprime mortgage borrowers, who defaulted in record numbers. The government injected $45 billion into Citi and guaranteed a $306 billion pool of toxic assets. Citi stock fell from $55 to 97 cents (pre-split).

To dig itself out, the bank needed boatloads of capital, which it raised in part by massive stock issuance. Before the financial crisis, Citi had 5.4 billion shares outstanding, which by 2011 ballooned to 29 billion shares. They traded in the low-single digits, which prevented some institutions from buying, as they were subject to rules against holding stocks under $5. To address this, Citi executed a 10-for-1 reverse stock split in May 2011. Through buybacks, Fraser has reduced shares outstanding to 1.8 billion—with more to come, she says.

Still, even at a 17-year high, Citi’s stock is the only major U.S. lender still trading below its pre-crisis peak.

Then came the “fat finger” imbroglio. In August 2020, Citi, as an administrative agent for Revlon, mistakenly wired $900 million to the cosmetics company’s lenders. Regulators were furious, fining the bank $400 million and issuing consent orders requiring Citi to rip up and replace its global risk platforms. That September, the bank said Fraser would replace CEO Michael Corbat. In July 2024, regulators fined Citi another $136 million for moving too slowly.

When Ray McGuire, the former longtime senior Citi executive who is now president of Lazard, was asked by Barron’s what was lacking at Citi during those lost years, he replied quickly and succinctly, “Leadership and courage.”

Those traits are exactly what Citi’s constituents are hoping Fraser is finally bringing to the table.

Helping her drive the bank’s recovery is Gonzalo Luchetti, a 20-year Citi veteran who was named chief financial officer in March. An Argentine with a Stanford University M.B.A., Luchetti previously led U.S. personal banking. Some analysts said he didn’t appear to have the credentials to replace Mark Mason, the longstanding and highly regarded CFO. Does Luchetti feel he’s in the hot seat?

“That’s exactly the way I like it,” he says. “They don’t know what I stand for and my values or what I can bring to the table. The results speak for themselves over time.”

Fraser has now organized the bank into five units: services, markets, banking, wealth, and U.S. consumer cards. A far cry from its financial supermarket days, it has exited most of its overseas consumer businesses and instead is focused on servicing the world’s biggest corporations and wealthiest individuals.

Services, which had a RoTCE of 28.6% last year, is Fraser’s “ crown jewel ,” helping thousands of multinational companies with trillions of dollars of daily transactions in some 190 countries around the world. Run by longstanding Citi banker Shahmir Khaliq, services isn’t a highflying, glossy business, but it’s an awfully good one, producing $7.1 billion of Citi’s $14.3 billion in income in 2025. Global tumult actually is a positive for this business,

Fraser says, as companies look to create new financial supply chains. “Services is knocking the cover off the ball,” says RBC’s Cassidy. “They’re a very recognizable, well-respected brand around the globe.”

Markets, which includes sales and trading, foreign exchange, and prime brokerage, drove some $22 billion in revenue last year, about the same as services. The unit is less profitable than services but is growing faster.

Banking, which includes old-school commercial lending and investment banking, grew 21% last year to $6.4 billion in revenue, with a RoTCE of 10.2%. In November, Fraser moved retail banking into the wealth group. That leaves U.S. consumer cards as a stand-alone business, in an effort to boost its standing in the competitive market for pricey, perk-promising credit cards .

Fraser looked to her two larger rivals, Bank of America and JPMorgan, for new, ambitious leaders in wealth management and banking. She found them in Andy Sieg , then the president of BofA’s Merrill Lynch wealth business, and Vis Raghavan , who ran investment banking globally at JPMorgan.

Sieg led Merrill to become one of the world’s dominant wealth managers. JPMorgan’s investment bank, Raghavan’s longtime home, often leads dealmakers’ league-table rankings. They are each charged with revitalizing business lines at Citi that have trailed rivals for years.

Both businesses are core to Fraser’s turnaround plans—and both face stiff competition. Citi’s wealth arm oversees $1.3 trillion in client balances, while Morgan Stanley and BofA handle $7.3 trillion and $4.6 trillion, respectively.

Asked about the wealth business, Fraser’s eyes light up. “Have you seen those results?” she says. “I’m happy with the direction it’s going in.”

Sieg has defined that direction and boosted returns. His team sold Citi’s trust business and private-market funds platform , handed asset-management responsibilities to BlackRock , and developed a new artificial-intelligence avatar concept for clients.

Moving Citi’s U.S. retail bank into the wealth business last fall surprised investors, even as it cemented Sieg’s influence over a broader swath of the bank. Meshing the two businesses together, the company says, should spur growth and turn more everyday banking customers into clients of the wealth business. Sieg aims to boost RoTCE to more than 20%, up from 7.6% last year and -2% in 2023.

By one closely watched measure, the business has had nowhere to go but up.

The wealth division’s efficiency ratio—a reflection of an organization’s spending relative to its revenue—was an exceptionally inefficient 99% when Sieg arrived in late 2023. It has improved to 79%.

“The business wasn’t operating like one global wealth business,” he says. “It was more akin to a collection of six or seven different businesses with a lot of self-contained, duplicative functions.”

Sieg’s leadership has been met with mixed reviews by current and former colleagues. A wave of wealth executives has left, and Sieg has brought in new blood from BofA, Morgan Stanley, and BlackRock. Ida Liu, Citi’s former longtime private banking leader, who had fostered relationships with wealthy families around the world, departed early last year as her business was reorganized.

Citi’s private bank has several thousand clients with an average net worth of some $500 million. Liu now runs HSBC’s private bank , which rivals Citi’s, particularly in Asia. Sieg had “mocked and undermined” Liu before she left the firm, Bloomberg News reported in August. At the time, Citi told Barron’s that Sieg has retained “industry-leading talent, including the more than 40% of accomplished women on Wealth’s senior leadership team.”

Citi hired law firm Paul Weiss to investigate complaints from several executives about Sieg’s behavior. Fraser says she is satisfied with the probe’s outcome and stands by Sieg. Asked to describe the nature of the findings, she told Barron’s, “We are in litigation at the moment, which I’m very happy to be. I’m not going to comment on that.”

In January, a former managing director at Citi accused Sieg of harassment in a lawsuit filed in the U.S. District Court for the Southern District of New York. Julia Carreon, a wealth management executive at Citi from 2021 until 2024, alleged that harassment she faced by Sieg and other leaders there fomented a hostile work environment and hurt her reputation. A Citi spokesman told Barron’s that the lawsuit “has absolutely no merit and we will demonstrate that through the legal process.” The bank later filed suit against Carreon .

Sieg said in an interview that complaints against him don’t fairly reflect his team’s culture. He said he has addressed complaints transparently with his leadership team and that “it’s not been something that has distracted me or our team.”

“I gave Andy a very tough change mandate—a very tough one,” Fraser said, referencing his responsibility to improve business performance. “I expect people wanting to be No. 1, to be winners, not to be content with second, third, or fourth place. There’s a lot of cultural change. There’s a lot of performance discipline and other elements that we drove through the firm. But Andy, in particular, had the biggest lift.”

Much like Sieg, Raghavan has a challenge in front of him to boost Citi’s investment bank. The business has lagged behind rivals in Wall Street assignments such as advising on mergers and acquisitions, losing out on lucrative business.

Raghavan, who is also responsible for setting companywide strategy, has hired several former colleagues into key roles at Citi. Former top JPMorgan banker Drago Rajkovic—“an iconic banker in [Silicon] Valley who is absolutely rooted in deal flow,” Raghavan said in an interview—joined Citi last year to co-lead M&A with Guillermo Baygual, also from JPMorgan. Raghavan tapped another former senior JPMorgan banker to co-lead technology investment banking. Several veteran Citi bankers, including the former global investment banking head, have exited.

Like the playbook at his former firm and across Wall Street, Raghavan wants to drive growth by engaging more with clients. Raghavan pointed to Johnson & Johnson , a longtime client of Citi’s cash-management and credit services that’s now tapping the firm for advice on big transactions. Citi is advising J&Jon its orthopedics business divestiture and advised on a $14.6 billion biopharmaceutical acquisition last year.

“What we are trying to do is get a united, single client focus,” he says. “We’re making sure that we have entrenched relationships—and that we are using the strength of the relationships to move beyond just the flow and the annuity needs to those clients’ episodic, strategic needs.”

Raghavan is seen by some as a polarizing executive whose communication has stung colleagues, people who have worked with him said. Bloomberg reported in September that “negative feedback about his demanding personality” had “helped rule him out from another more senior banking position” while at JPMorgan.

“We’re thrilled to have Vis as a member of Citi’s executive management team and proud of the business he is building here,” a Citi spokesman said.

Asked to describe his leadership style, Raghavan told Barron’s, “I am very direct [and] speak what’s on my mind.” He added that on his team, “there is honesty and an openness and willingness on everyone’s part to feed off each other and take this cause to greater heights.”

With new executives in place, and improving results, Citi’s stock has already jumped 85% in the past year alone. Is it too late for investors to buy in? Not to Wall Street. Analysts overwhelmingly call it a Buy, with zero Sell ratings, per FactSet. They argue that Citi can grow earnings sustainably and that it has wrestled expenses under control.

“There is so much upside,” Fraser says. “We have unique strengths in our global footprint. The role we play in global payments really cannot be replicated. We are only just getting started in using our scale and our advantages. We’re cheap. Get on the train.”

When asked about her legacy, Fraser says it’s too early to consider, but she would like to be recognized as a “leader in my own right—not just the first woman.” Still, she would like “to see a lot more women thriving in the industry, because we can add a lot of value.”

And as Citi shareholders can tell you, it’s all about adding value.