The Super Prime Credit Score Club Is Growing Rapidly -By Oyin Adedoyin, WSJ

The ranks of super prime credit-score holders have grown by 15 million over the last half-dozen years, thanks in part to young people.

Americans with top-tier scores above 780 have been a boost to banks, which are increasingly courting high-end customers with offers of credit cards and other loans. Banks touted their focus on customers with strong credit while reporting first-quarter earnings growth in recent weeks.

“With our portfolio heavily weighted to prime, delinquencies and credit losses declined and are well in line with expectations,” said Jane Fraser , Citi group’s chair and chief executive, on an earnings call.

Approximately 85% of the bank’s balances are extended to consumers with a FICO score of 660 or higher.

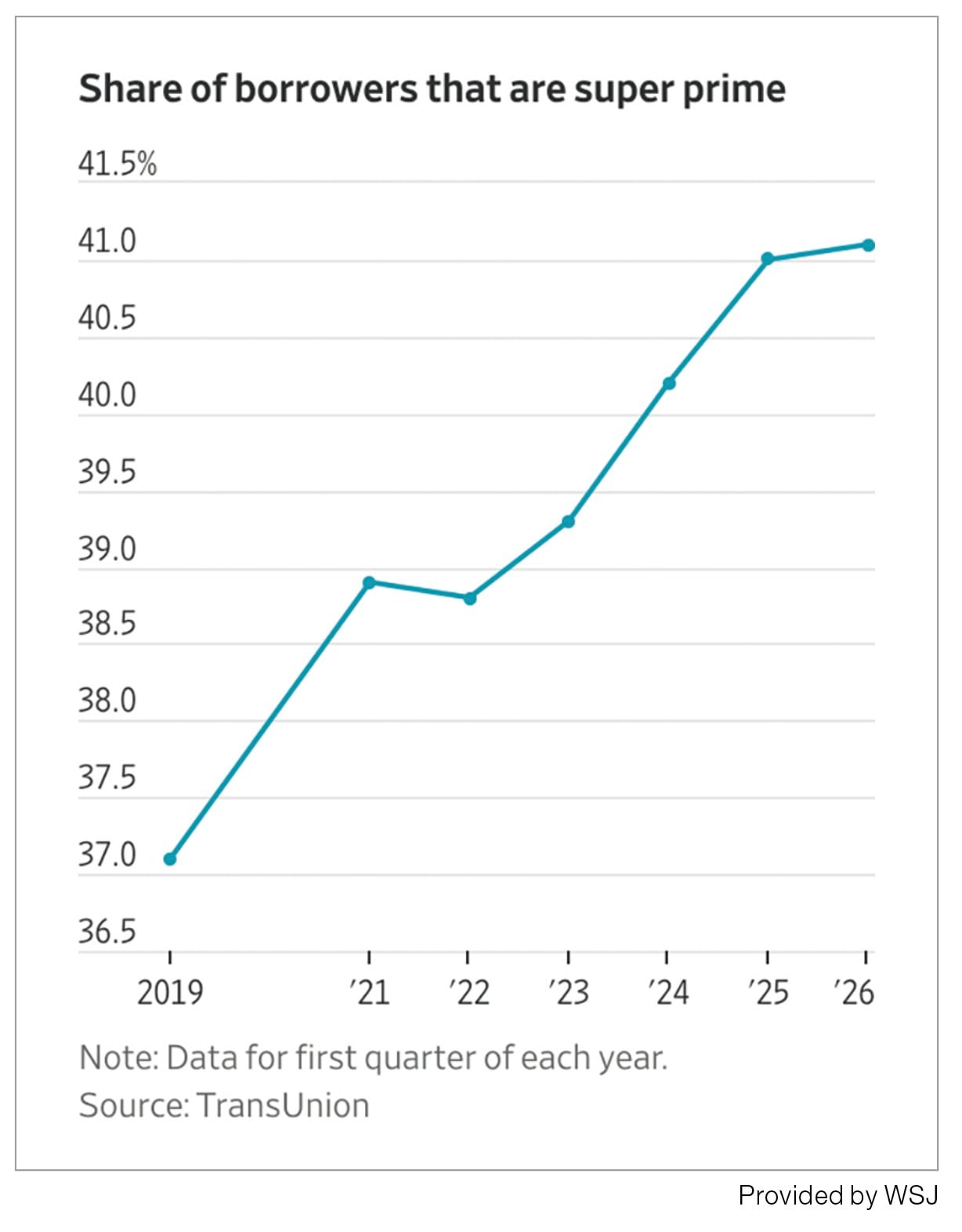

Lots of consumers entered the super prime category during the pandemic when they received stimulus payments or cut back on spending, according to TransUnion , a credit-reporting firm. The growth continued as worker incomes have risen, and stocks and home values surged.

More than 41% of consumers with a balance had super prime credit scores in the first quarter of this year, up from 37% six years earlier, according to TransUnion’s data.

Many of the people entering into this category are Gen Z consumers who grew up with greater awareness of their credit scores and the financial decisions that can lift them, according to credit-reporting firms and card companies. Monitoring and improving credit scores has become something of a national obsession.

That means a shifting mix of people who are taking the premium credit cards and rewards products that banks are giving priority to. They are typically reserved for people with high credit scores, credit-card executives say.

“The younger generation is more equipped for the changing dynamics in the world today than, in fact, maybe more middle-aged people,” said Stephen Squeri , CEO of American Express , in an earnings call. “I feel a lot more comfortable having a card base that is skewed a little bit younger than what you used to see 10 years ago.”

Most of the new American Express accounts acquired last quarter were for fee-paying products like their premium credit cards. The company said that Gen Z and millennial account acquisition continued to rise as younger adults outperformed older generations in credit metrics.

The consumer spending that powers the U.S. economy is increasingly driven by the growing upper-middle class and richer. For them especially, incomes have risen faster than inflation, The Wall Street Journal has reported.

On the other end of the spectrum, credit-card debt has risen to a record $1.3 trillion and more people are falling behind on payments, suggesting growing stress in an increasingly bifurcated economy. That stress has also appeared in auto-loan delinquencies and home foreclosures.

The share of people with subprime credit scores has remained roughly flat over the past six years.

Gen Z is the most variable generation when it comes to financial health. For all of their gains, the share of those with weak finances also grew by 10% between the second quarter of 2023 and the fourth quarter of 2025, according to credit-reporting firm Equifax. In comparison, the number of Gen X consumers with low ratings of financial strength grew by 11%, the largest increase across all generations.

Lenders are providing smaller credit lines to consumers with lower credit scores. For those who are near prime, average credit-line limits for new cards per consumer rose 5% between the third quarter of 2019 and 2025, according to TransUnion. For super prime consumers, credit-line limits increased 11% within the same time frame.

“The U.S. consumer remains resilient in the aggregate but increasingly bifurcated beneath the surface,” said Charles Scharf , CEO of Wells Fargo , in an earnings call.