Private Credit's Exposure to Ailing Software Industry Is Bigger Than Advertised-By Jack Pitcher and Matt Wirz , WSJ

Many private-credit fund managers are playing down their exposure to software as fears spread about threats from artificial intelligence. A detailed analysis revealed four large funds marketed to individual investors by Apollo Global Management , Ares Management , Blackstone and Blue Owl Capital have more exposure to the software industry than their filings suggest.

Investors’ concerns about the industry’s software exposure helped prompt record withdrawals from private-credit funds in the first quarter. Fund managers contend that AI will affect each software company differently and that some will adapt or even benefit.

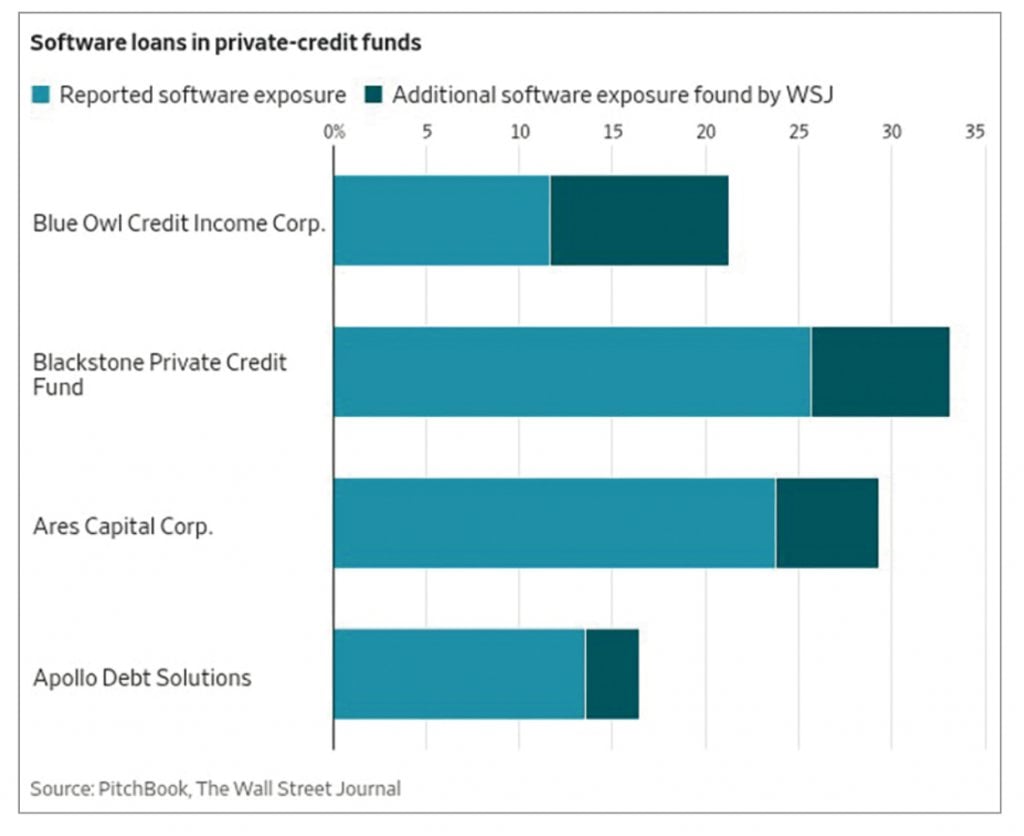

The Blue Owl Credit Income Corp. fund had nearly twice as much exposure to software as it reported, an analysis by The Wall Street Journal found, while the discrepancies for the other funds were smaller. On average, the four funds classified about 19% of their investments as software, while the Journal found their average software exposure to be about 25%.

Private-credit funds provide an industry breakdown of their loans to companies each quarter. Software is the biggest category for most of them. Methodologies for categorizing loans vary. Ares said in a filing that it adheres to the independent Global Industry Classification Standard, while others use different methods.

“The way in which [private-credit funds] classify their sector exposures is not uniform,” Barclays analysts said in a report Thursday about stresses in the private-credit market. “This sector ‘massaging’ generates concern from the investor community and makes it difficult to assess degrees of true diversification across funds.”

Private-credit funds say software companies that serve other sectors, such as healthcare, should be reported in those buckets because of their dependence on the industries. That approach predates the recent investor anxiety around software.

The Wall Street Journal reviewed the breakdowns in four of the largest private-credit funds, which make high-interest loans to companies. The Journal used sector tags from data provider PitchBook and its own analysis to identify software-focused companies within private-credit portfolios. It presented each of the fund managers with a list of loans to companies it identified as software companies that the funds didn’t identify as such.

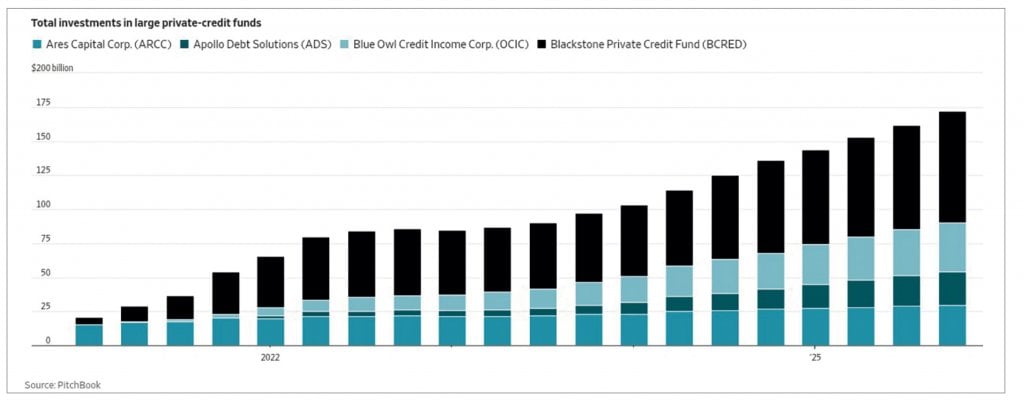

The Journal found that the two funds that grew fastest in the cohort—those of Blackstone and Blue Owl—had more software exposure in other industry buckets. Some in the industry worry the funds’ rapid growth could hurt the quality of their portfolios. Private-credit fund managers depend heavily on a supply of loans from private-equity buyouts, which were concentrated in software companies over the past five years.

The Journal’s analysis found that:

•The Blue Owl Credit Income Corp. fund said that 11.6% of its portfolio consisted of loans to “internet software and services” companies at the end of the fourth quarter. The Journal found its software exposure to be around 21%.

•The Blackstone Private Credit Fund, known as Bcred, reported 25.7% in software at the end of the third quarter, while the Journal found roughly 33% exposure.

•Ares Capital Corp. reported 23.8% in “software and services” at the end of the fourth quarter, while the Journal found nearly 30% exposure.

•The Apollo Debt Solutions fund reported 13.6% in software in the fourth quarter, while the Journal found a roughly 16% exposure.

•Blue Owl’s fund categorized loans to 47 software-focused companies in other buckets ranging from education to transportation. Eight of the companies, including one with software in its name, BMC Software, were described as “business services.”

•One of the Blackstone fund’s biggest investments, over $1 billion of loans to Inovalon, was categorized as “IT Services” and not included in its software exposure. Inovalon describes itself on its website as “a software company that empowers healthcare organizations.”

•One of Ares’s biggest loans was to Symplr Software, which Ares described in a filing as a software-as-a-service, or SaaS, provider. But because Ares relied on the Global Industry Classification Standard, the loan wasn’t counted in the fund’s reported “software and services” exposure. It fell under “health care equipment and services” instead.

•Different fund managers categorized the same company in different buckets. Blackstone has always counted Forterro as software, while Apollo classified the company as “technology hardware, storage & peripherals” before reclassifying it as software late last year.

As unease about AI replacement crushed the stocks of public software companies in recent months, some fund managers played down their concentration in the industry or turned the spotlight on competitors. The software companies in private-credit portfolios have higher debt compared with their earnings, on average, than companies in any other sector, according to a recent Morgan Stanley analysis.

“If you look at the private-credit deals that have gone sideways, there’s a software element to the majority of them,” said Alex Chaloff , chief investment officer at Bernstein Private Wealth Management.

Many private-credit fund managers say they believe that fears about software loans are overblown and that they feel good about the quality of their portfolios.

Blue Owl touted its technology investing chops for years and helped pioneer private-credit lending to SaaS companies. After the so-called SaaSpocalypse hit markets in January, the tune appeared to change.

“We’re not negative in any manner on software,” Blue Owl Co-Chief Executive Marc Lipschultz told analysts on a conference call in early February, before pointing out that for the Credit Income fund “ actually amongst the peer group, we have the lowest software exposure.”

Some fund managers have altered which companies they include in the category. One of the largest investments in Apollo’s fund is a $239 million loan to Anaplan, a self-described SaaS provider. But the fund recorded the loan as an IT investment for almost three years before changing it to software in March of 2025. The fund reclassified at least two other loans to software in the fourth quarter of 2025.

Write to Jack Pitcher at [email protected] and Matt Wirz at [email protected]

免責聲明:本專頁刊載的所有投資分析技巧,只可作參考用途。市場瞬息萬變,讀者在作出投資決定前理應審慎,並主動掌握市場最新狀況。若不幸招致任何損失,概與本刊及相關作者無關。而本集團旗下網站或社交平台的網誌內容及觀點,僅屬筆者個人意見,與新傳媒立場無關。本集團旗下網站對因上述人士張貼之資訊內容所帶來之損失或損害概不負責。