Is Another Financial Crisis Lurking in Private Credit? -By Greg Ip , WSJ

For those with long memories, news that some private credit funds have capped withdrawals brings to mind the summer of 2007, when a European bank limited withdrawals from funds stuffed with securities linked to subprime mortgages. The global financial crisis had begun.

Like subprime, private credit in just a few decades went from niche to major asset class. And like subprime, private credit is opaque, mostly unregulated and connected to other parts of the financial system including banks.

So do private credit’s troubles herald a systemic shock similar to what we saw two decades ago? With the caveat that crises are inherently unpredictable, probably not. The 2007-09 crisis was one of the worst in history, and that alone militates against something as bad.

That said, the crisis taught us which vulnerabilities to watch for in the financial system. Private credit exhibits enough for us to scrutinize what could go wrong, especially in a broader shock such as rising oil prices and interest rates.

Private credit usually refers to a loan by a nonbank lender to a private business (i.e., whose shares aren’t listed on the stock market). Like subprime, it grew up in the shadows of established finance. Private-equity managers such as Apollo Global Management and KKR started arranging the loans that finance leveraged buyouts. Endowments, pension funds and the like then invested in the loans.

One parallel between subprime and private credit is opacity. Unlike bonds, private credit isn’t regulated by the Securities and Exchange Commission—though some private-credit funds, such as business-development companies, are—and unlike bank loans, isn’t overseen by the Federal Reserve or other bank regulators. This is a feature, not a bug: Financial innovation is often an adaptation to regulation. Private credit benefited from postcrisis rules that made bank loans costlier.

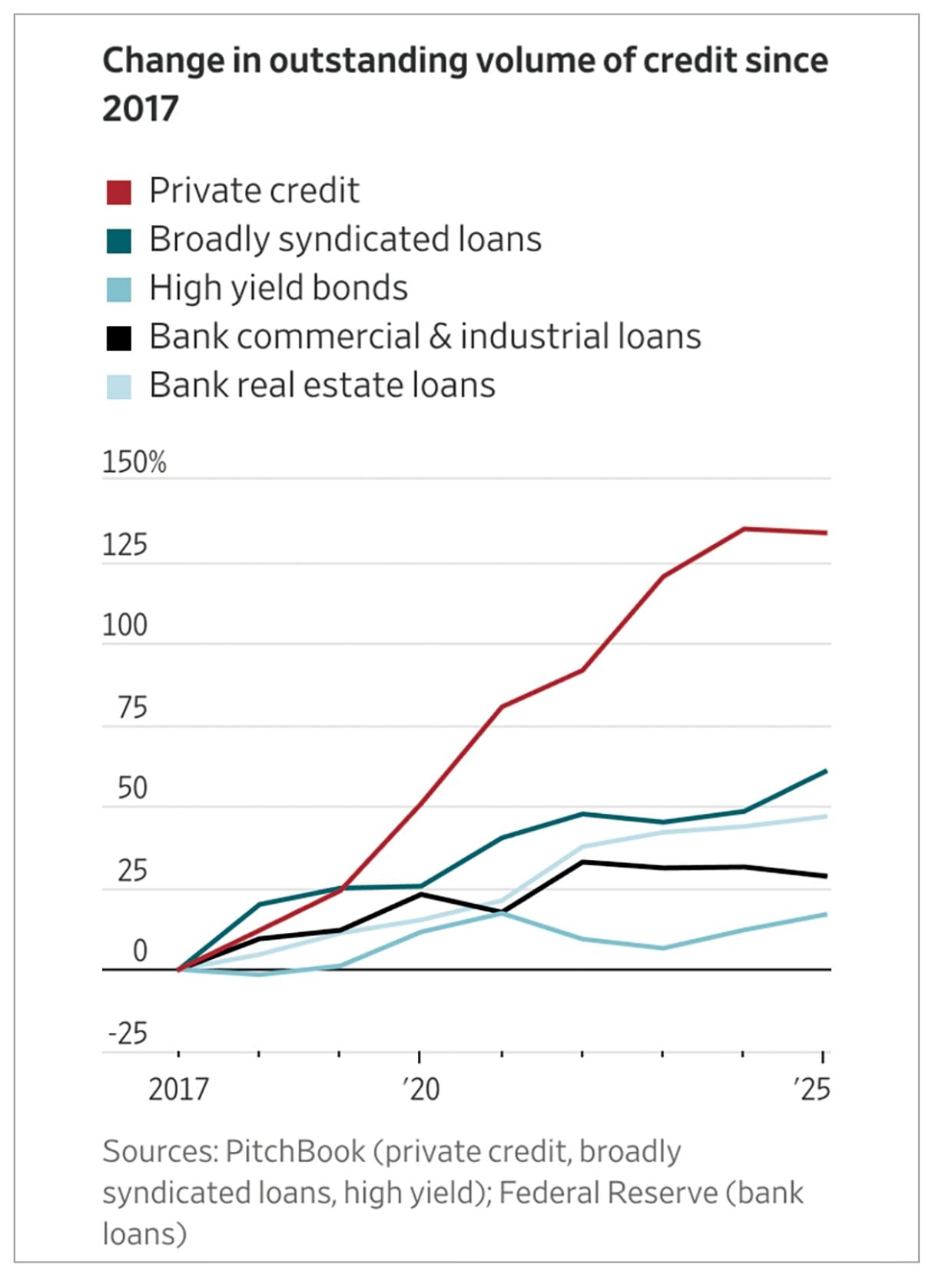

But this opacity means there is no agreed-on way to define, measure or categorize private credit. PitchBook estimates that total private credit in the U.S. has tripled since 2015 to $1.3 trillion, including “dry powder” (available, unused capital). Preqin, a unit of BlackRock, itself a major private-credit manager, puts the North American total at $1.6 trillion. Some analysts toss out figures north of $2 trillion, but those usually cover the whole world.

By PitchBook’s measure, private credit is almost as big as syndicated loans ($1.5 trillion), which banks originate and then distribute to investors, and high-yield bonds ($1.8 trillion). Banks’ commercial, industrial and real-estate loans total nearly $6 trillion. Private credit is comparable to subprime, which at its peak totaled roughly $1.5 trillion, about 15% of all residential mortgages, though that was much larger relative to the economy.

As subprime once did, private credit diversifies the economy’s financing channels. “Instead of credit simply coming from the banking sector, the fact you can spread risk…to the full spectrum of the financial system is a plus,” said Fabio Natalucci , who monitored financial stability for the International Monetary Fund and now heads the Andersen Institute for Finance and Economics.

Yet, as with subprime, private credit has become intertwined with other financial players, in particular banks and insurance companies. “This interconnectedness could come back as a weakness,” Natalucci said.

Interconnectedness can propagate and amplify losses through the financial system. Banks, securities dealers, hedge funds, Fannie Mae , Freddie Mac and the insurer American International Group nearly collapsed because of their exposure to subprime-linked loans, securities or derivatives.

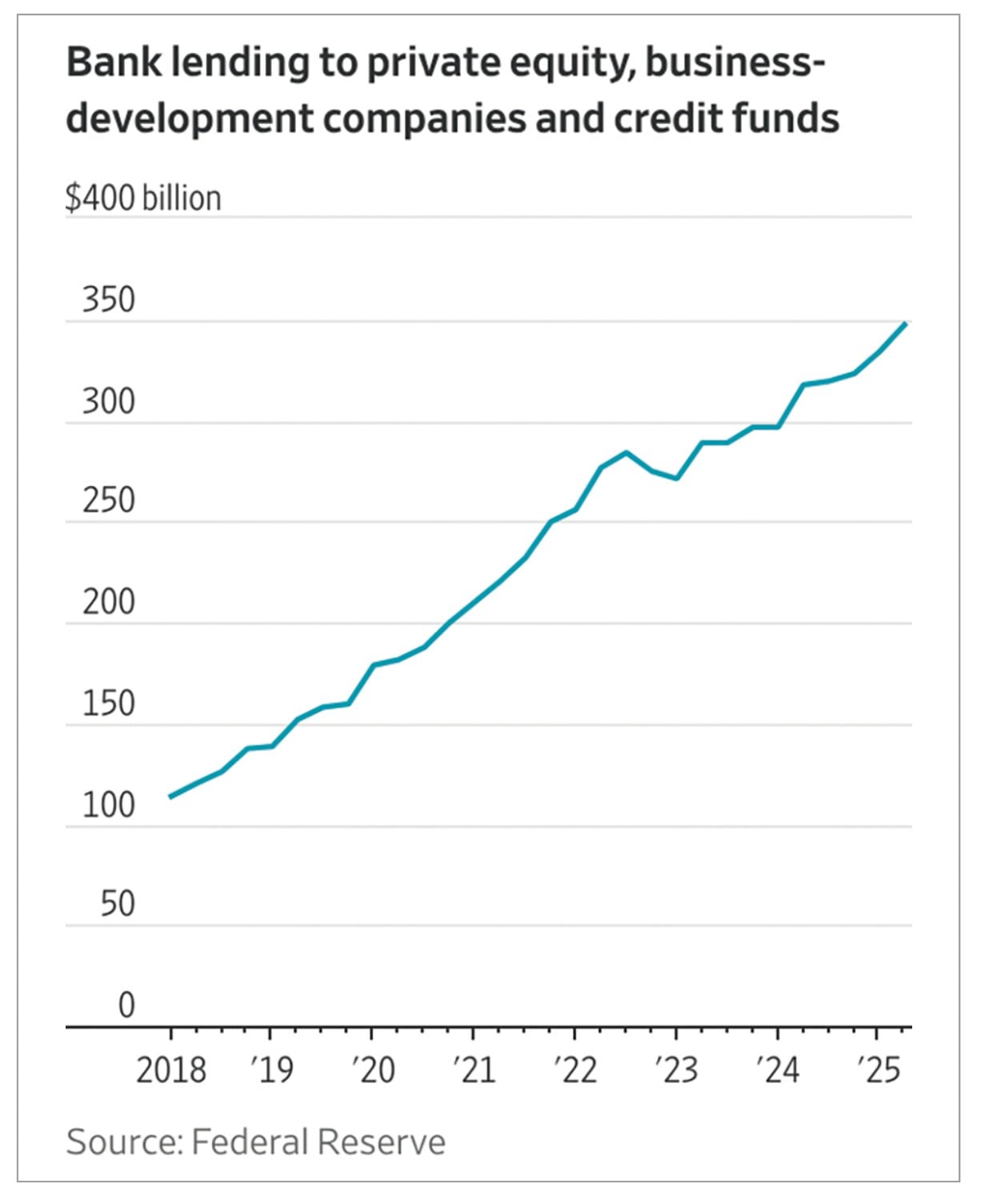

Banks have tripled lending to private equity and credit since 2018 to over $300 billion, part of a broader expansion of lending to financial companies. As a result, funds that invest in highly leveraged companies have themselves become leveraged.

To be sure, banks’ exposure is small relative to their total assets. Many have protected themselves through “synthetic risk transfers,” under which they retain the loan but pay someone such as a hedge fund to take the hit if the loan defaults. The IMF estimates that banks worldwide have transferred the risk on $1 trillion of assets (not just private credit) this way.

Nonetheless, this ties private credit more closely to other parts of the financial system. For example, a hedge fund might borrow from one bank to take on the credit risk from another bank. These linkages raise “potential contagion risks,” the IMF said.

Life insurers are big investors in private credit, raising several red flags. Many have borrowed to finance their purchases. Some are owned by the private-equity firms, such as Apollo, which originated the loans. They are overseen by state insurance commissioners , who lack the resources and broader mandate of federal bank regulators. This past fall the IMF warned of inflated credit ratings on life insurers’ private credit holdings, which could result in defaults far exceeding predictions in a downturn.

For all the similarities, the differences between subprime and private credit are just as important. Subprime was more leveraged, and more complex. The loans were typically bundled into mortgage-backed securities, also known as MBS, which were then sliced up into tranches of differing risk. The MBS were in turn bundled into collateralized debt obligations, or CDOs, and sliced up again. Then, “synthetic” CDOs were created by writing derivatives linked to CDOs or MBS. These levels of leverage magnified losses.

Some private credit is packaged into collateralized loan obligations , or CLOs, but they are far smaller and less complex than their subprime forerunners.

The institutions that originated and held subprime debt financed themselves with short-term IOUs. When lenders became nervous, they stopped rolling over those IOUs, the equivalent of a run on a bank. This caused fire sales of securities, driving down values and spreading the losses.

Private credit is much less “runnable.” Unlike mutual funds, credit funds don’t allow investors to redeem their shares at any time. Some funds aimed at retail investors allow periodic redemptions up to a certain cap. Withdrawals recently hit those caps at funds managed by BlackRock, Morgan Stanley, Apollo and Cliffwater. But such funds only amount to 6% of total private credit, according to PitchBook.

Because private-credit loans don’t trade, their true value is unknowable until they mature or are sold. If investors lose faith in what fund managers claim the loans are worth, withdrawals could accelerate, forcing managers to sell loans, driving values down further.

Subprime, by fueling a massive loosening of credit, became a key driver of housing, and when subprime lending dried up, that killed the housing market and the broader economy. Private credit hasn’t fueled any comparable bubble in business borrowing. If the sector shrinks, businesses have ample alternative sources of credit.

Don’t take too much comfort from that. The private-credit boom has been part and parcel of a broader embrace of risk. Lenders everywhere might have grown lax, which is why fraud-related defaults at some financial companies have rattled bank stocks . An economic shock such as high oil prices could expose fragile borrowers across several markets, private credit included.

The default rate on private credit has drifted up from between 4% and 5% a year ago to between 5% and 6% now, according to Fitch Ratings.

Natalucci said: “If people have doubts about underlying credit quality when the economy is growing like this, a slowdown in the economy because of the [Iran] conflict is going to add to those credit concerns. Even if it doesn’t become a financial crisis, it could become an amplifier of the slowdown.”

免責聲明:本專頁刊載的所有投資分析技巧,只可作參考用途。市場瞬息萬變,讀者在作出投資決定前理應審慎,並主動掌握市場最新狀況。若不幸招致任何損失,概與本刊及相關作者無關。而本集團旗下網站或社交平台的網誌內容及觀點,僅屬筆者個人意見,與新傳媒立場無關。本集團旗下網站對因上述人士張貼之資訊內容所帶來之損失或損害概不負責。